This article was originally published on the Access+ portal for ByrdAdatto Access+ members on October 14, 2019. Enjoy this free access to learn more about the C Corp.

Traditionally avoided by many small businesses and startups due to the adverse impact of “double taxation”, the subchapter “C” corporation[1] (“C Corp”) is finding new ground with entrepreneurs and business and practice owners. One of the driving factors in entity selection is tax treatment at the federal level as well as the state level. And until recently, C Corps have long received little consideration among small business owners and startups in favor of a pass-through tax structure. There are, however, a number a reasons why a C Corp may be a viable choice in certain circumstances.

Three general strategies for which the C Corp may be a preferred choice are as follows: (1) the medical entity in an management services organization (“MSO”) Model, (2) Mid-Term Exit Strategy, and (1) Venture Capital Fund Raising. There is overlap among all three of these strategies. The MSO Model could be included under Venture Capital Fund Raising or the Mid-Term Exit Strategy, and seeking to raise funds through venture capital (“VC”) or private equity is often integral to a Mid-Term Exit Strategy or the MSO Model. While there are other reasons for considering the C Corp, this article will focus on the three general categories as outlined above.

Get more great content with Access+.

Structural Background

Many do not realize that when forming an entity, typically there are two principle filings. The first filing is at the state level, which actually forms the company as a legal entity. The second filing(s), which is the primary focus of this article, is with the Internal Revenue Service to obtain an Employer Identification number (“EIN”) and otherwise elect how the new entity will be treated from a federal tax perspective. Clients and tax and legal professionals alike routinely confuse entity structure and tax classification with another, e.g., stating an entity is taxed as an LLC (i.e., a Limited Liability Company). There is no such tax classification as an LLC. An LLC is purely a state level entity structure, which may elect to be taxed as any of the following classification outlined below (excluding a sole proprietor)[2]. What they mean to say, however, is that the entity is taxed as a partnership when they say is taxed as an LLC. Understanding the difference can alleviate a lot of confusion.

C Corps

A corporation is a form of entity structure created at the state level, the ownership of which is represented by shareholders owning the corporation’s shares of capital stock. A corporation may be taxed at the entity level (i.e., a C Corp) or on a pass-through basis at the shareholder level (i.e., a subchapter “S” corporation). Accordingly, the “C” corporation designation is merely a federal tax classification where the company will be taxed based on its corporate income.[3] Most companies that are publically traded on the stock exchanges are C Corps; however, publicly traded companies constitute less than one percent of all U.S. businesses.[4] Approximately 92% of private businesses in the U.S. are structured from a tax perspective as pass-through entities such as partnerships, subchapter “S” corporations, and or a sole proprietorships.[5]

S Corps

A subchapter “S” corporation[6] (“S Corp”), is federal tax classification where the corporation itself is not taxed at the entity level, but income, losses, deductions, and credits are passed through and taxed at the shareholder level[7] based on each shareholder’s own tax bracket. S Corps, however, have a number of limitations, which may affect their feasibility when selecting this structure for a new business. Shareholders may only be natural persons, certain types of trusts, estates, and certain exempt organizations (such as a 501(c)(3) nonprofit), but cannot be partnerships, corporations[8], or non-resident aliens.[9] Further, an S Corp may have no more than 100 shareholders all of which must be US citizens or residents.[10] The company may have only one class of stock with profits and losses allocated in proportion to each shareholder’s percentage interest of ownership in the S Corp.[11] Moreover, the company must not be an “ineligible corporation” such as an insurance company subject to subchapter L of the Internal Revenue Code, domestic international sales corporation, or a financial institution, which uses the reserve method of accounting for bad debts described in Section 585 of the Internal Revenue Code.[12]

Partnerships

Like an S Corp, partnership taxation is on a pass-through basis. Partnership taxation is codified as Subchapter K of Chapter 1 of the U.S. Internal Revenue Code (Title 26 of the United States Code)[13]. Pass-through taxation means that the partnership does not pay taxes on its income. Instead, the partners pay tax on their “distributive share” of the partnership’s taxable income, even if no funds are distributed by the partnership to the partners. The partnership must file an annual information return to report the income, deductions, gains, losses, etc., from its operations, but it does not pay income tax. Each partner includes his or her share of the partnership’s income or loss on his or her tax return.

Federal tax law permits the owners of the entity to agree how the income of the entity will be allocated among them, but requires that this allocation reflect the economic reality of their business arrangement, as tested under complicated rules. Furthermore, partners cannot be employees and should not be issued a Form W-2. The partnership must furnish copies of Schedule K-1 (Form 1065) to the partners by the date Form 1065 is required to be filed, including extensions. Arguably, partnership tax has the most complicated set of tax laws, rules, and regulations.

Sole Proprietorships

Another pass-through tax structure is the sole proprietorship. A sole proprietorship is the simplest and unfortunately from the legal perspective of the respective small owners, the most common structure chosen to start a business. It is an unincorporated business owned and run by one person with no distinction between the business and the sole proprietor. The owner is entitled to and taxed on all profits. Furthermore, the owner is personally responsible and liable for all the business’s debts, losses, and liabilities. And for that reason alone, no person should operate a business as a sole proprietorship.

The owner reports the business’s income, losses and expenses with a Schedule C and the standard Form 1040 personal tax return. The “bottom-line amount” from Schedule C transfers to the owner’s personal tax return and it’s the owner’s responsibility to withhold and pay all income taxes, including self-employment and estimated taxes.

The MSO Model

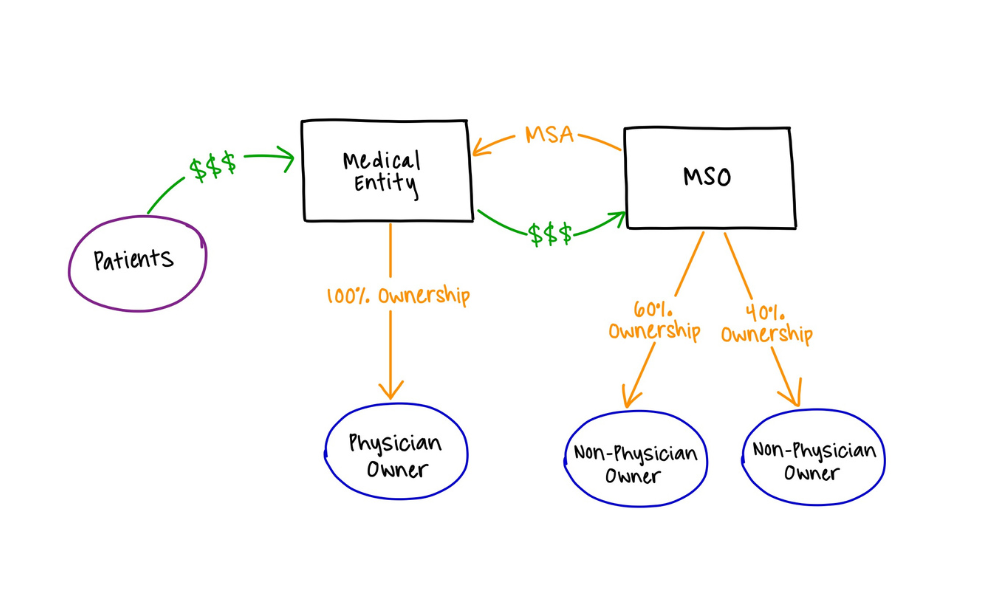

The basic setup of the MSO Model is for one entity to act as a management services organization (“MSO Entity”) to provide management services to a physician owned entity (“Medical Entity”). Though the patients will experience treatments as if they are in one business, there will actually be two businesses involved in the arrangement.

The use of a C Corp for the medical entity in the MSO Model can be a useful structure to avoid unintended messiness on the physician owner’s tax return. The concept behind MSO structure is to create a separation between the clinical side of a medical practice and the business side of the practice. There are a number of reasons to separate these two aspects of a practice. They include asset protection as well as creating a vehicle through which non-licensed parties may participate in the economics of a medical practice.

The MSO Entity will provide non-medical management services. The non-medical services provided by the MSO Entity can include marketing and branding, billing and collecting, patient coordination, record keeping, accounting, payroll, space and medical equipment leasing, and ordering non-medical supplies. The MSO Entity would enter into a contract called a Management Services Agreement (“MSA”) with the Medical Entity, which would govern the relationship between the parties. The Medical Entity would pay the MSO Entity a monthly management fee for all of the services the MSO Entity provides to the Medical Entity.

Through the fees paid to the MSO Entity, a substantial amount, if not all of the profit from the Medical Entity could flow to the MSO Entity. This allows non-physicians to participate in the business and essentially receive the entire economic benefit as if they owned the Medical Entity.

MSO MODEL

A drawback of this model, assuming that it is structured and otherwise operated in compliance with applicable laws, is that if the Medical Entity is a pass-through entity for tax purposes (i.e., S Corp, partnership, or disregarded entity), the physician owner will have all the revenues and expenses flow through to the physician. As you will see in the model above, patient revenues must initially flow into the Medical Entity. The physician commonly plays a clinical role but not a risk taking entrepreneurial role in the model. If, for example, a physician agreed to be paid $3,000 per month to own the Medical Entity and supervise and delegate to the providers of the Medical Entity, neither the physician nor the non-physician MSO owners will likely want all the revenues and expenses showing up on the physician’s personal tax return. If the Medical Entity is taxed as a C Corp, however, the entity would file its own tax return and would not flow through to the physician. Because the entity pays taxes and any dividends to the owner would effectively cause double taxation on the same revenues, this is an important filter. However, other than compensation paid to a physician owner, the Medical Entity should not make profits. All revenue will essentially be washed out by deductible expenses (including the management fee). And in our example above, the intent is to push all income to the MSO Entity so there would be no dividends paid thus eliminating the double tax issue.

If the goal in an MSO structure is to push most or all of the income to the MSO Entity from the Medical Entity, a C Corp may be the preferred tax structure to select for the Medical Entity.

Mid-Term Exit Strategy

Most startup owners tend to choose the LLC taxed as a partnership (or some other pass through tax structure). While LLCs taxed as partnerships have been a dominant entity choice for years for startup owners, recent changes in tax laws have created a new impetus to consider the C Corp.

President Trump’s 2017 Tax Cuts and Jobs Act[14] along with an expansion of Section 1202 of the Internal Revenue Code[15] under the Obama Administration have created an advantageous strategy for using the C Corp as a startup vehicle in certain situations. This strategy works best from an economic perspective when the business does not intend to distribute profits in the form of dividends during the early years as the business is in growth mode.

For a person looking to start a small business, retain earnings within the business for working capital and growth, and have at least a medium term exit strategy, a C corporation may be the way to go. Provided the owner holds the stock in the C Corp for at least 5 years and follows certain technical rules, the owner will not pay capital gains tax on the sale of the stock on gains the greater of up to $10 million or 10 times the original investment under Section 1202.[16] The idea in this scenario is that the entity pays corporate income tax on profits in the early years (which is a lower rate than personal tax rates), not make any dividends to the owners (to avoid double taxation issues), and potentially achieve zero taxes on the sale (if structured appropriately).

With most any startup, everyone is waiting for a positive exit, which will typically take one of two forms: (1) acquisition by a larger company, or (2) an initial public offering (“IPO”). In both situations, the investors end up selling their equity and profiting from the difference between their investment amount and their sales proceeds. So if an investor invested $100,000 in a startup and sold it for $1,000,000 after holding the equity for at least one year, the investor would pay capital gains tax at 20% on the $900,000 gain or $180,000. However, if the startup was formed as a C Corp and the investor purchased Common or Preferred stock and held the stock for at least 5 years, the investor would pay nothing in taxes on the gain!

Venture Capital Fund Raising

It goes without saying how critical adequate startup and growth or expansion capital is for a new or young business. If the business’s founders intend to look for funding from venture capitalists, however, it may be prudent to form a corporation taxed as a C Corp.

A corporation taxed as a C Corp is often recommended to those who will seek venture capital funding because many VC firms will not invest in LLCs or cannot own S corporations since VCs are not eligible to own shares in an S Corp. Moreover, the governing documents of many VC firms prohibit them from investing in LLCs. This is due in part since any equity-like features have to be custom drafted into the Operating Agreement of an LLC each time in order to approximate the stock-like functions of a corporation, which is not appealing to VCs. Sophisticated professional investors such as VCs often have portfolios with dozens or even hundreds of holdings. If LLCs are among their holdings, VCs are required to deal with these varying Operating Agreements on an individual basis.

Moreover, VCs prefer corporations taxed as C Corps for many reasons, which include the following. Many VCs do not want the business’ income to pass through to them as would be the case with partnership taxation. VCs would rather the entity pay the tax. Furthermore, VCs often have tax-exempt investors, which could run into tax problems if business income were passed through to the owners of the VC firm. Additionally, VCs may want the business to be able to offer stock options to management and key employees to attract, retain, and incentivize key talent, which is much more feasible with a C Corp. LLCs taxed as partnerships cannot offer incentive stock options and their “profits interest” counterpart that they can issue in an effort to mirror stock are complex and more costly to structure and manage than stock options.

C Corps offer a better exit strategy since their stock tends to be more liquid with VCs selling their interest to a third party or having an initial public offering. Both options are easier with a C corp. And only C Corps can shield $10 million plus in capital gains taxes upon exit. Further, VCs are more familiar and comfortable with corporations and because there is such a large body of well-developed case law, which is not the case for LLCs.

Proper entity choice, however, depends upon other factors and not just whether venture capital funding may be sought, If there is a strong possibility or certainty of VC funding, a corporation taxed as a C Corp may be the best choice.

Conclusion

Of course, there are many other considerations and factors that must be considered when structuring an entity and a C Corp still may not be the best option for many small business startups. Along with the short and long-term goals and strategies, careful legal and tax considerations should be addressed with legal and tax counsel to optimize the selection. Furthermore, the Democratic Party is seeking to repeal President Trump’s tax changes and significantly increase personal income tax rates, which could jeopardize this strategy in the future. Nevertheless, the C Corp is more of a feasible option to consider for many startups or small business as a result of the recent changes in tax law. And even without the changes, it remains the preferred choice if venture capital will be sought.

ByrdAdatto represents businesses, physician practices, dental practices, law firms, medical spas, and other companies throughout the United States. For more information and guidance on the subject, please contact us at info@byrdadatto.com.

[1] 26 USC §§ 301-391 (Subchapter C – Corporate Distributions and Adjustments).

[2] Cf. Disregarded Entity tax clarification for single owner LLC, For income tax purposes, an LLC with only one member is treated as an entity disregarded as separate from its owner, unless it files Form 8832 with the IRS and affirmatively elects to be treated as a corporation. For purposes of employment tax and certain excise taxes, however, an LLC with only one member is still considered a separate entity

[3] 26 USC § 11.

[4] https://www.nber.org/digest/apr07/w12354.html

[5] https://www.investmentnews.com/article/20180608/FREE/180609896/pass-throughs-versus-c-corporations-under-the-new-tax-law

[6] 26 USC §§ 1361-1379 (Subchapter S – Tax Treatment of S Corporations and Their Shareholders).

[7] 26 USC § 1366.

[8] See exception for a qualified subchapter “S” subsidiary (“QSub”), which is a subsidiary corporation 100% owned by an S Corp that has made a valid QSub election for the subsidiary, 26 USC § 1361(b)(3)(B).

[9] 26 USC § 1361(b).

[10] Id.

[11] Id.

[12] Id.

[13] 26 USC §§ 701-761 (Subchapter K – Partners and Partnerships).

[14] https://www.govinfo.gov/content/pkg/PLAW-115publ97/html/PLAW-115publ97.htm.

[15] 26 USC § 1202.

[16] 26 USC § 1202(b)(1).